July ECB Meeting And Gold

Last week, the European Central Bank released its most recent monetary policy statement. What does it imply for the gold market?

Prologue: Draghi’s Speech in Sintra

We have already covered Thursday’s ECB monetary policy meeting. However, it was an important event which significantly moved the financial markets – and which could potentially exert a huge impact on the gold market in the near future. This is why we decided to dig into the topic today.

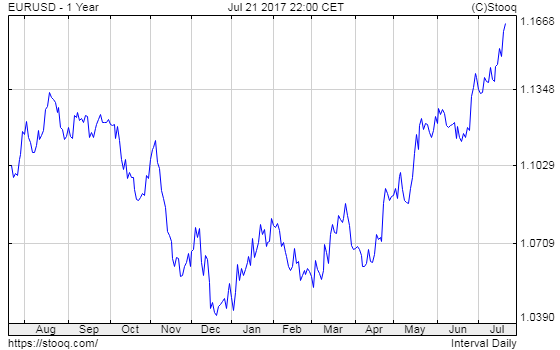

To understand the importance of the recent ECB meeting we have to go back to Draghi’s speech in Sintra, Portugal on June, 27, which was interpreted as a hawkish turn. Draghi said then that “the threat of deflation is gone and reflationary forces are at play.” Investors considered these remarks a signal that the ECB would start to tighten its monetary policy in the near-future. They over-reacted a bit and both the German bond yields and the euro soared on tapering concerns, as one can see in the chart below.

Chart 1: EUR/USD exchange rate over the last year.

Why do we think that the traders over-reacted? Because they decided to ignore the dovish part of Draghi’s speech. He also said that “inflation dynamics are not yet durable and self-sustaining. So our monetary policy needs to be persistent”, and this is why “a very substantial degree of monetary accommodation is still needed for underlying inflation pressures to build up, and to support headline inflation in the medium term.”

Drama: July ECB Meeting

This is why the recent meeting was long awaited and investors looked for any signals about the ECB’s future actions. Interestingly, Draghi did not provide any hawkish hints about the tightening of monetary policy. Some analysts even considered his remarks dovish. Nonetheless, the euro further rallied, while the price of gold jumped, as the chart below shows.

Chart 2: Price of gold over the three last days.

It seems that the recent monetary policy statement and Draghi’s answers to questions during the press conference did not damp the hawkish expectations. All this in spite of the fact that Draghi pointed out that inflation had remained at subdued levels and, hence, reiterated that “a very substantial degree of monetary accommodation is still needed for underlying inflation pressures to gradually build up and support headline inflation developments in the medium term.”

If these expectations are fulfilled, the consequences may be huge. So far, the Fed has been the only hawk in town. In July, the Bank of Canada joined the U.S. central bank and hiked its key policy rate for the first time in seven years. The Bank of England and the ECB may be next in line. If this scenario is realized, the divergence in monetary policies adopted by major central banks would narrow, which should exert downward pressure on the U.S. dollar. The depreciation of the greenback would be bullish for gold.

Epilogue: What Can We Expect from The ECB Now?

Draghi did not specify the timing of the ECB’s decision about the fate of its quantitative easing program. He only said that a discussion on that topic should take place in the fall. Some investors bet on September, but they may be disappointed. The second quarter wage data will be available after the September meeting. And we should not forget that it would be just two weeks before the election in Germany. Hence, October seems to be the most likely date for a decision on the future of the ECB’s monetary policy stance. It may be the key time for the gold market. As a reminder, the Fed’s announcement of its intention to taper quantitative easing made the U.S. dollar rally in 2014. The same may happen to the euro. If the EUR/USD exchange rate rises, gold prices should also rally. Surely, there is plenty of time until October and a lot may happen, causing ups and downs in the gold market. And a possible ECB tapering would be very dovish. Still, in the fall we may experience an important fundamental shift in the global monetary policy – and long-term investors should not neglect it. Stay tuned!

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our trading alerts.

********

Arkadiusz Sieroń is the author of Sunshine Profits’ monthly Gold Market Overview report, in which he keeps subscribers up-to-date regarding key fundamental developments affecting the gold market and helps them prepare for the major changes. Arkadiusz is a certified Investment Adviser, a long-time precious metals market enthusiast, and a Ph.D. candidate. He is also a Laureate of the 6th International Vernon Smith Prize. You can reach Arkadiusz at Sunshine Profits’ contact page.

More from Gold-Eagle.com: