What Affects the Price of Gold?

A Historical Perspective

Gold has been a part of the human story since the dawn of civilization. One part store of wealth, one part ornament, and one part modern technology, gold stands at the crossroads of multiple financial, religious, and industrial trends.

What actually drives the price of gold? Is it fear of currency devaluation or stock market crashes? Is it war? Or is it jewelry and electronics fabrication?

The answer is many-fold. In this article, we will highlight the complex and inter-related drivers for gold prices worldwide so that investors may have a fuller understanding of the totality of the precious metals market.

Gold Supply and Demand

Fundamentally, the answer to what affects the price of gold is the same as for every other market: supply and demand.

Yet the supply and demand balance for gold, a market which dates back to the dawn of record-keeping itself, is itself largely driven by factors which are deeply ingrained in the human psyche.

Two extreme emotions – greed and fear – comprise the spectrum through which the majority of participants in the gold market make their buy and sell decisions.

In this article we will examine the many ways in which greed and fear play out, over and over again, in the most ancient of financial markets which is yet seeing new life today.

Gold Supply

Before we examine the actual numbers, let us consider one important preliminary supply factor for gold: this is the only element in which all of the supply ever mined in the history of the world still exists above ground. Gold never rusts, tarnishes, corrodes, or burns. Except for small amounts which may have been lost in shipwrecks at the bottom of the ocean or disposed of in landfills, all of the gold that has ever been brought to surface of the planet still exists in one form or another (and arguably, those two sub-components are retrievable as well).

Gold is unique in this way: neither oil, copper, silver, nor fiat currencies share this indestructible property – all of these items are permanently consumed or degraded in some way throughout time.

Thus, all of the gold mined in humanity’s history still exists. Indeed, it is estimated that 187,000 metric tonnes of gold have been mined in the history of our species. As one metric tonne equals just over 32,150 troy ounces, we can calculate that approximately 6 billion ounces of gold have been brought to the Earth’s surface through humanity’s collective efforts.

An interesting statistic to note is that as the world’s population now stands at 7.6 billion people, there exist above ground roughly 0.79 ounces of gold for each human being alive today. Our population has been increasing at an average rate of 1.2% over the last decade (though declining recently). Meanwhile an average of 2,886 metric tonnes or 92.8 million ounces of new gold have been brought to earth’s surface each year. This represents an average supply increase of approximately 1.5% per year.

Thus, the natural rate of human population growth is comparable to the worldwide mining extraction rate for new gold. As we will examine later in this article, this natural supply limit in relation to human population growth is one of the key defining properties which has served to keep gold’s value relatively stable throughout time.

The Raw Gold Supply Numbers

With this knowledge of total new gold supply growth versus total human population growth being roughly equal, let us dive deeper into the actual supply numbers for gold. To form the basis of this section, we will analyze with what is considered the “gold standard” of industry metrics, the Thompson Reuters GMFS annual gold survey (original link: http://financial-risk-solutions.thomsonreuters.info/GFMS). For the analysis that follows, we will consider average statistics from the past decade and note any trend changes that are observed in recent years.

As we can see above, highlighted in red, an average of 2,886 metric tonnes of gold have been extracted from the earth’s crust each year over the past decade, a number which has been steadily growing and with 2016 showing the highest on record at 3,222 tonnes. This mine supply is the total new amount added to the 187,000 tonnes mined in the history of our civilization.

Although mine supply for gold has seen new records in recent years, the valuation of the gold mining industry itself is presently near multi-decade lows. The relative valuation of the mining industry versus gold bullion is the topic featured in the article The Trade of the Decade.

The second line-item on the supply side can be deceiving: scrap supply is recycled supply, which is typically derived from the melting down of gold found in old jewelry, electronics, and dental applications. While this scrap, once melted and refined, is available for purchase in the market each year, it is not new supply as referenced by the world’s total above-ground stock. New supply comes only from mine production.

To reiterate the most important points on gold supply: nearly all of the existing above-ground gold ever mined is potentially available to the market, and new supply is limited by an amount roughly equivalent to human population growth.

Gold Demand

Gold demand is the more complex side of the equation. There are two questions which must be examined side-by-side when we discuss demand for gold:

-

Who are the major purchasers of gold?

-

What drives the psychology of each category?

These two questions are related but distinct. Let us examine these questions for each sub-section that follows.

Gold Jewelry Demand

It may surprise some who are used to considering gold as a financial asset to learn that the single largest demand component worldwide comes from jewelry. Indeed, the numbers confirm: on average, 2,229 metric tonnes of gold were purchased annually in jewelry form over the past 10 years. This represents over 53% of the average demand.

Even more significant, of that 53% of the gold market going each year to jewelry, over half is purchased by two countries alone: China and India. Yes, the demand for gold in Asia is that strong.

In sum then, 28% of the entire world’s annual gold demand comes from Chinese and Indian jewelry buyers. That is quite the cohort.

Yet it would be erroneous to believe that all of this jewelry-buying is simply for ornamental purposes. Especially in India, where the tradition of gifting and wearing 24-karat gold during the fall wedding season remains strong, what is clear is that jewelry purchases often serve as wearable investments:

The takeaway is that jewelry purchases from India and China remain the single largest demand segment for gold to this day; this demand consists of both ceremonial and investment motives. We can never overlook these two countries and the history behind their respective traditions when it comes to evaluating gold price trends.

Gold Industrial Demand

Industrial demand is a small yet critical component of the total gold equation. Gold is the third-most conductive element for electrical current, behind silver and copper. Yet because it never corrodes, gold is often used when for electrical components when longevity is the foremost concern.

Due to its extreme malleability and non-toxic nature, gold is also used in small quantities in dentistry, in the form of alloy fillings.

Highlighted below in green, we can see that annual average industrial demand over the preceding 10 years has been 432 metric tonnes, or 10% of total demand, and falling slightly in recent years. Gold is becoming used less in industry as new technologies result in cheaper alternatives, but some industrial gold demand will remain a reality for the indefinite future:

Important trends can be observed when we measure the relative valuation of gold versus the rest of the industrial commodities. For example, this can tell us whether gold is rising in price due to industrial activity worldwide, or whether a premium is being placed on gold for its historical monetary role. While industrial gold demand remains near 10% of total demand in recent years, a more detailed study of the relationship between the precious metal and other commodities can be found in the article Gold versus Commodities.

Central Bank Demand

Central bank demand for gold has been highly variable over the past decade, but with a trend that is increasing. For 2016, 257 metric tonnes of gold were purchased in sum by central banks.

As we can see in the statistics, central banks became net purchasers of gold in 2010 for the first time in over a decade. In past years, central banks had been net sellers of gold.

At this point in the demand equation, a question arises: why do central banks purchase or sell gold at all? What motivates the desire to accumulate gold as an asset when – in the modern age for the first time in recorded history – not a single government currency is officially backed by gold?

The saying “actions speak louder than words” could not be more fitting.

Indeed, what we see through the act of central bank gold purchases over the past decade is that the historical monetary metal is still considered important – albeit unofficially – to the backing of national currency regimes.

Why is gold considered valuable as an anchor to currencies? Let us now consider the properties which have made gold an ideal store of wealth for millennia.

Gold As Money

Throughout the recorded history of civilization, gold has uniquely served as the most common form of high-powered money. This phenomenon has occurred through no central planning decree or government fiat – instead, gold has emerged as money through the collective decisions of the world’s diverse citizens throughout countless generations. Indeed, the “broad market” has chosen gold to serve as money over the millennia, after many other forms to store value have been tried and failed.

What are the properties which make gold better-suited for money than other forms, either elemental or human-created?

Properties Which Make Gold Money

No other element shares the confluence of the following properties:

-

Extremely rare – the total quantity of all the gold ever mined in the history of humankind would fit snugly into the center court of a tennis match.

-

Extremely divisible – a single ounce of gold can be drawn into a wire 80 kilometers (50 miles) long, five microns, or five millionths of a meter, thick.

-

Never rusts, tarnishes, corrodes, or burns – gold is the least reactive of all metals. Gold may be lost at the bottom of the ocean for 1,000 years and upon retrieval, will not have deteriorated due to any chemical interaction.

-

Has never been worth zero – in contrast, every fiat digital or paper currency ever invented by government or central banks has eventually become worthless. For example, we see below the purchasing power of the US dollar since the founding of the Federal Reserve in 1913:

Purchasing power of the US dollar, 1913 – present.

While there are some who would argue that gold is no longer needed in modern currency systems due to advances in technology or human ingenuity, it is worth remembering that every single non-backed currency that has ever existed has eventually declined to its intrinsic value, which is zero. To propose the idea that the present un-backed monetary system worldwide will escape this fate would require us to utter what are considered the four most dangerous words in investing: “This time is different.”

Ironically, the fact that not a single currency is today backed by any tangible commodity means that the majority of the world’s citizens are implicitly stating this risky phrase. To this day, it is estimated that less than 1% of the western population own any gold whatsoever. The thesis for a gold price advance in the future thus comes from the scenario that if even a small percentage of the world’s population re-awakened to the properties that make gold uniquely suited for a store of value, the price would be forced significantly upward to compensate.

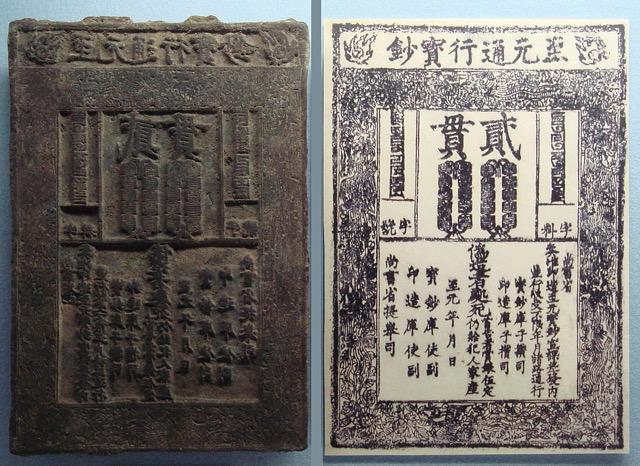

The earliest known fiat money: Yuan dynasty banknotes, China, 13th century – became worthless within 50 years of initial printing.

Back to the Central Banks

Government issuance of national currencies dates back thousands of years, yet is it only in the last 47 years that not a single currency worldwide has been officially backed by gold.

In the United States, from the founding of the country in 1776 through 1933, the price of gold was officially set at approximately $20 per troy ounce, with only slight variations over the 157 years.

In the midst of the Great Depression, President Roosevelt outlawed the private ownership of gold, via Executive Order 6102, and proceeded to devalue the dollar so that the same ounce of gold was now represented by $35 dollars. Gold did not change – it was the dollar that was devalued approximately 75%.

In the years following World War II, the Bretton Woods Agreement set the US dollar as the world’s reserve currency, with a value maintained at $35 per ounce of gold. Every other major world currency was subsequently tied to the value of the dollar. In essence, the world remained on a gold standard.

The international system held until 1971, when President Nixon officially severed the link between gold and the US dollar, following the unsustainable spending of the Vietnam War and simultaneous domestic social programs. Thus, starting in 1971 and for the first time in modern history, not a single currency in the world had any official backing. This was an unprecedented situation – and it remains today.

We can therefore state that for the past 47 years, the world has been living through an experiment of monetary history. Let us emphasize: this is the first time in the history of civilization that not a single government currency is backed by gold.

Why, then, do central banks continue to purchase gold? Why spend currency on an asset which sits in a vault when instead that currency could go to improving infrastructure or helping citizens?

The answer lies somewhere deep in humanity’s development. Human civilization has emerged concurrently with gold as the anchor of monetary systems for millennia. The only way that we can explain the modern split between official central bank policy which claims that gold is not a reserve asset and the simultaneous purchasing of gold to be held in national vaults is to say that there is something deeply ingrained in the human psyche which instinctively knows that gold is the single premier store of value.

Laws and policies may come and go, but somewhere deeper the human consciousness we know that gold stands unique for its unwavering ability to store value over thousands of years. Modern central bank purchases of gold demonstrate an instinctive drive to hold never-failing wealth in an era of unprecedented political instability.

Other Gold Investment Demand

Whereas central banks buy gold to back their balance sheets whether officially recognized or not, investment demand from private participants takes on a more diverse set of motives.

Below we highlight the major (dark green) and sub-component (light green) sections which comprise worldwide investment demand for gold outside of wearable investments (jewelry) and central bank purchases.

The first component of investment demand consists of retail investment, which is sub-divided into bars and coins. This component has averaged 1,179 metric tonnes per year over the past decade, with large variability.

The second major component is ETF (exchange-traded fund) demand. This category consists of dozens of funds worldwide which trade on major international exchanges and allow investors to own a claim to gold, without having to take physical delivery of the actual coins or bars. ETF demand is also highly variable, with an average of 141 metric tonnes purchased annually over the past decade, although 2016 showing the first positive year since 2012.

The final component to investment demand comes from futures exchange inventory build. Typically a smaller and highly variable segment, this demand comes from purchases and sales of registered gold inventory due to the settlement of contracts from several worldwide futures exchanges, including those in New York, Tokyo, and Shanghai. Average annual demand has been seen at 4 metric tonnes for the past decade, although again it is highly variable from year to year.

Notably, volume on futures exchanges has broken quarterly records in 2017 for the highest volume of all time. Large investors are clearly still interested in purchasing gold.

In sum, a total of 1,324 metric tonnes have been demanded per year on average in the multiple private investment categories over the past decade.

What Impacts Gold Investment Demand?

What are the drivers behind institutional and individual purchases of gold for investment purposes?

Being the sum of millions of participants, the reasons are necessarily diverse. But if we were to divide the demand into several major categories, they would be seen as follows:

Inflation / Currency Hedge

Gold is incredibly stable as a store of value over the long-term.

Former Chairman of the Federal Reserve, Alan Greenspan, is quoted as saying in 1966:

“In the absence of the gold standard, there is no way to protect savings from confiscation through inflation. There is no safe store of value… Deficit spending is simply a scheme for the confiscation of wealth. Gold stands in the way of this insidious process. It stands as a protector of property rights.“

As an example, an old saying dates back hundreds of years: “An ounce of gold can buy a nice men’s suit and pair of shoes.” And indeed, this still holds true today: at roughly $1,300 one ounce of gold one can buy a nicely-tailored men’s suit, and a fine pair of shoes. Such is an example of how gold can hold its value over extremely long periods of time, as countless depreciated fiat paper currencies from past centuries would not buy the button on a man’s shirt today.

Over shorter periods, the relationship is more difficult to predict. For example, we can observe periods in which gold has protected an investor from a decline in the currency. For example, note below how from 2000 – 2008, as the US dollar lost 40% of its value, gold rose 300% to compensate. Indeed, gold can oftentimes rise a greater percentage than the local currency loses value, as investors flood into the relatively tiny gold market for protection en masse.

We can observe weakness in the US dollar over recent months in 2017 and 2018, and our analysis shows that a continued decline is expected into 2019. Will gold continue to rise in an opposite manner as the dollar? This article highlights the case: US Dollar on the Edge – How Will It Affect Gold Prices?

Yet the challenge for gold investors is that the precious metal is not perfect as a currency hedge over short and intermediate time periods. For example, below we show the period from 1987 – 1992, during which time the US dollar lost 13% of its value while gold simultaneously lost 33% of its value.

The takeaway is that gold serves as an effective hedge in the long term against fiat currency depreciation, but it wavers in its ability to do so over shorter timeframes.

Geopolitical Hedge

Gold often serves as a hedge against geopolitical instability over the short term, and indeed, tends to spike in the days and weeks preceding the real or perceived threat of a war or terrorist attack. The key takeaway for precious metals investors to understand, however, is that isolated geopolitical price spikes for gold generally do not alter the long-term trend already in place for the metal. Long-term trend analysis allows us to place the geopolitical price spike into proper context.

For example, let us consider the most significant terrorist attack of our lifetimes and how gold responded on September 11, 2001.

9/11 Terrorist Attacks

September 11 was a Tuesday, and on the day of the actual attacks, gold spiked from $273 per ounce to $290, a 6.2% increase. In today’s terms at $1,300 gold, that would equate to an $80 intraday spike. The price action in the year leading up to the attack and in the months following is shown below:

Note how after the September 11 surge, gold topped three weeks later just below $300 per ounce. Moreover, in the two months that followed, as fears of an apocalypse-scenario faded, gold gave back all of its gains. Specifically, on November 24, gold closed below $272, which was the opening price from the morning of 9/11.

Many investors who bought gold in the days following the attacks were surely frustrated to be sitting on losses within a few months, and those who did not put this price action into proper trend analysis likely sold and moved on from the precious metals altogether.

How did the isolated terrorist-attack spike in the price of gold relate to the overall trend? This is a key point of consideration.

Broader Technical Perspective

Let us back out the above chart for increased perspective to examine the trends that were in play at the time. Below we show gold from 1997 – 2002. The same 9/11 geopolitical price spike is again highlighted:

It is important to remember that gold had been declining for almost two decades prior to 2001, and the last five years of the decline took the shape of a cup base pattern, so called for its resemblance to the bottom of a rounded tea cup (blue annotation).

Further, gold had seen significant multi-year downtrend breaks leading up to the 9/11 price spike, shown above by the red callouts.

A double-bottom was observed in April 2001, matching within a few dollars the July 1999 price of $252 per ounce.

In sum, gold was showing several classic technical indicators hinting that a trend change from the prior years of falling prices was in progress. The September 11 terrorist-related price spike, while it was given back over the following two months, was itself actually part of a longer basing formation for the price of gold in the late 1990’s and early 2000’s.

Longer-Term Perspective

How did the “isolated” September 11 price spike look when viewed within the context of the bull market which unfolded over the next 10 years? The following chart speaks for itself, where the spike can barely be seen amidst the more significant bottom that served as a launching pad for the next decade.

The takeaway regarding geopolitical instability and gold prices: gold will often spike in the days and weeks preceding a major geopolitical event, such as a terrorist attack and/or threats of war. However, geopolitical price spikes will generally be short-lived. The underlying primary trend in gold prices, whether higher or lower, will be the primary determinant for the precious metal over the subsequent years after the immediate fear reaction inevitably subsides.

Hedge Against Conventional Assets

Gold will often – but not always – benefit from an increased flow of funds during times in which conventional assets, such as stocks and bonds, experience declines.

Let us examine some examples. First, note how during the 2000 – 2002 bear market in stocks following the bursting of the NASDAQ dot-com bubble, as the stock market fell by over 50%, gold increased by 12%. Not only did holders of gold avoid all losses in the stock market, but they actually profited above and beyond holders in cash at the time:

However, investors should know that in the most intense periods of stock market panic, gold does not always act as a safe-haven. For example, let us examine the most severe portion of the stock market crash in 2008, in which the US S&P 500 fell by over 40% within a period of six months. Note how during the worst of the crash, gold actually fell simultaneously with stocks, albeit by a lesser 23%.

The point is that in a true stock market panic, as margin calls force traders to sell anything and everything in order to cover their other losses, gold may be sold simultaneously with other asset classes.

By most valuation measures, the US stock market is now on par with the most overvalued in history. Will gold again rise as stock prices fall? Recent history suggests yes, as this article discusses: US Stock Market Signs of a Top.

Gold Investment Demand Summary

Gold has seen an average of 1,324 metric tonnes demand per year for the past decade across three areas of the private investment: physical bars and coins, ETFs, and exchange inventory.

Investment demand is highly variable year over year. The investment demand for gold generally occurs for one of three purposes: inflation / currency hedge, geopolitical hedge, and conventional asset hedge.

Gold holds its value exceptionally well over long periods, but is never perfect in its hedging capability across shorter timeframes. Its ability to protect investors depends primarily on the underlying psychology of the markets at the time, which can be observed by studying the larger technical trends which are in effect.

Conclusion: What Affects the Price of Gold?

The price of gold is determined by supply and demand, the same as every other market in the world. Supply and demand are, themselves, functions of two of the most basic of human emotions: fear and greed.

Yet gold is unique amongst markets in that new supply extracted from the Earth is inherently limited, its extraction rate being roughly equivalent to new population growth on a year-over-year basis.

Meanwhile, all of the gold ever mined in the history of humankind is generally available to the market, albeit at widely variable prices and circumstances.

Gold demand is strongly driven by jewelry purchases out of India and China – yet jewelry in Asia is significantly the form in these countries that investment takes.

Worldwide, gold has limited yet irreplaceable functioning in electronics and industrial fabrication.

In recent weeks, gold has seen increased safe-haven investment demand as United States and China have engaged in an escalating series of trade wars.

Yet the most significant form of demand in western nations comes from institutions, private individuals, and even central banks who purchase the asset due to its function as a lasting store of value. We are living during a monetary experiment which has never been tried before on a worldwide basis, in which not a single currency is backed by any gold whatsoever. Private ownership of gold thus takes on increased importance.

At various times, gold performs better or worse as a hedge against fiat currency depreciation, against geopolitical risk, and against declines in conventional asset classes. Investor psychology is the most significant factor which determines how gold will perform over any short or intermediate time period. We strongly encourage investors to pay strict attention to the overall trends in market direction, as gold may move opposite to how conventional wisdom would suggest for years at a time and at certain critical turning points.

Ultimately, the reason why humankind has gravitated toward gold over the millennia as the pinnacle store of value is because of its natural properties: limited supply, resistance against corrosion, rust, and fire, extreme divisibility and portability, and lustrous aesthetic beauty. Gold is not perfect as a store of value – but it is the best that humankind has discovered yet. And in an era where for the first time in recorded history not a single government currency is linked to any tangible asset, the need for gold as a store of value is greater than ever. With only 0.79 ounces of gold available above ground for every man, woman, and child alive today, it would not take more than a small portion of the world’s population to wake up to this age-old wisdom for the price of gold to be forced upward by a multiple of its present value.

“Gold is the money of kings; silver is the money of gentlemen; barter is the money of peasants; but debt is the money of slaves.” – Norm Franz, 2001.

********

Gold-Eagle provides regular commentary and analysis of gold, precious metals and the economy. Be the first to be informed by signing up for our free email newsletter.

Christopher Aaron began his career as an intelligence analyst for the CIA and Department of Defense. He served two tours to Afghanistan and Iraq between 2006 - 2009, conducting pattern-of-life mapping for military leaders.

Mapping shares similarities with technical analysis of the financial markets because both involve the interpretation of repeating patterns found in human nature. He is the founder of iGold Advisor, providing research on the precious metals, and iGlobal Analytics, featuring technical analysis of the global capital markets.

Christopher speaks regularly on the cyclical patterns found within the financial markets and on international policy. He has been featured in the New York Times and NPR news amongst other publications.

More from Gold-Eagle.com: